Traditional 401(k) vs Roth 401(k): Which Option Is Right For You?

Breaking down the differences between your employer sponsored retirement plan options

Many employers that offer a 401(k) actually have two types of plans for you to choose from.

A traditional 401(k)

A Roth 401(k)

Let me explain each and how to find out which is the best option for you:

What Is A 401(k)?

A 401(k) plan is one of the most popular options when it comes to saving for retirement. These plans allow you to automatically contribute a portion of your paycheck into an investment account that grows over time. Many employers offer a 401(k) as a benefit to their employees, and it can be a great way to automate your retirement savings.

But there’re actually two different types of 401(k) plans to choose from. Let me explain the differences between a traditional 401(k) and a Roth 401(k) to help you decide which option is best for your unique financial situation.

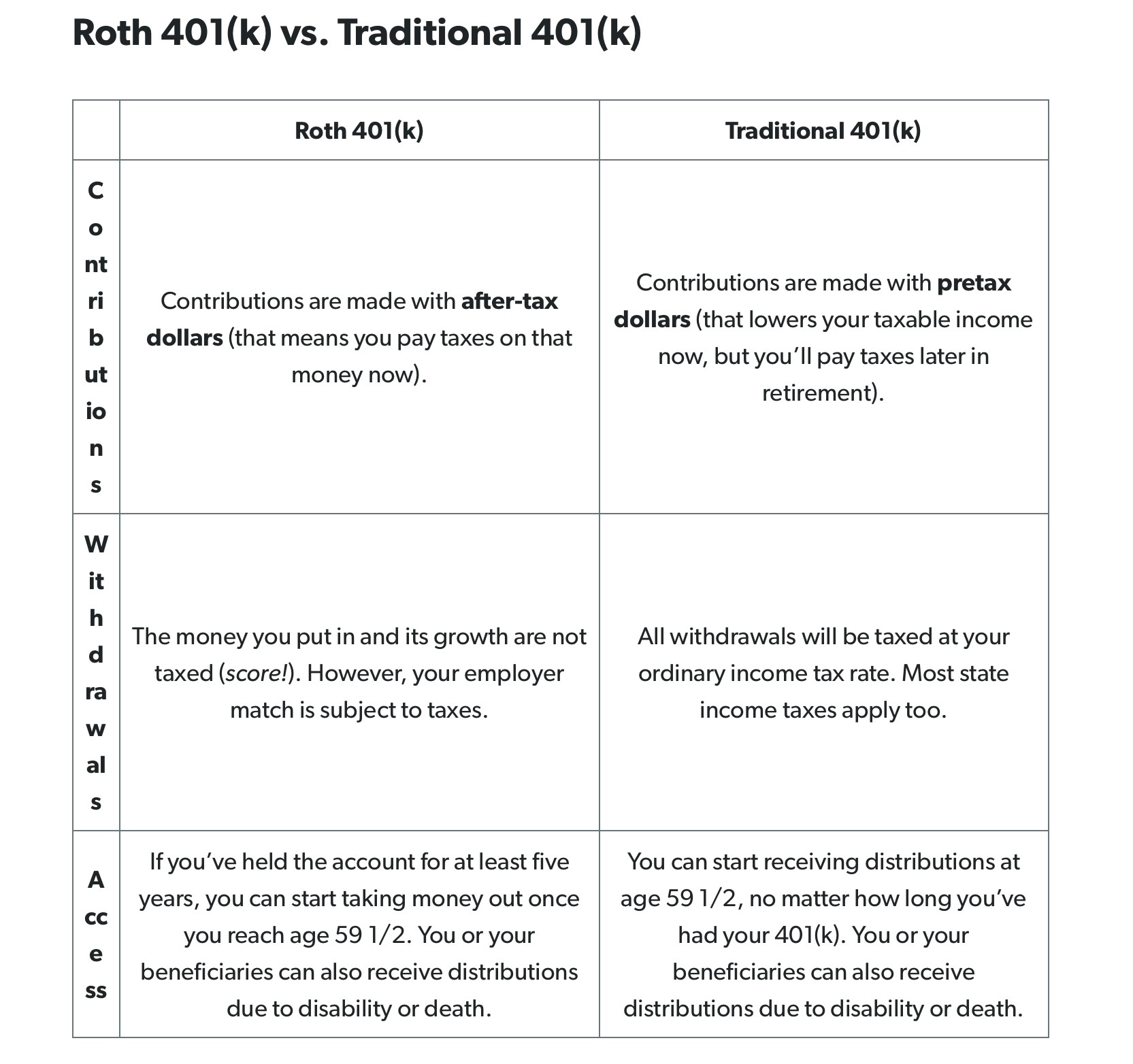

Traditional 401(k)

Let's start with the traditional 401(k). This plan allows you to make pre-tax contributions to your retirement account, which means the money you contribute is deducted from your taxable income.

For example, if you earn $50,000 per year and contribute $5,000 to your traditional 401(k), you'll only pay taxes on $45,000 of income. That can be a significant tax savings, especially if you're in a higher tax bracket.

The downside to a traditional 401(k) is that you will have to pay taxes on your contributions and any investment earnings when you withdraw the money in retirement. This is known as "tax-deferred" growth, meaning you're deferring taxes until a later date.

If you're in a lower tax bracket in retirement than you are now, you may end up paying less in taxes overall. However, if you're in a higher tax bracket in retirement, you could end up paying more in taxes than you would have if you had chosen a Roth 401(k).

Roth 401(k)

Now let's talk about the Roth 401(k). This plan allows you to make after-tax contributions, which means you pay taxes on your contributions now, but your withdrawals in retirement are tax-free.

For example, if you earn $50,000 per year and contribute $5,000 to your Roth 401(k), you'll pay taxes on the full $50,000 of income. But you won't have to pay taxes on your contributions or any investment earnings when you withdraw the money in retirement.

The benefit of a Roth 401(k) is that you're essentially locking in your tax rate now. If you think you'll be in a higher tax bracket in retirement, a Roth 401(k) could be a smart choice because you'll avoid paying taxes on your withdrawals when you're in a higher tax bracket. Additionally, because you've already paid taxes on your contributions, you won't have to worry about tax bills eating into your retirement savings.

An Important Factor To Consider (Matching Contributions)

One important thing to keep in mind is that some employers offer matching contributions to their employees' 401(k) plans. For example, your employer may match 50% of your contributions up to a certain percentage of your salary. This can be a great incentive to participate in your 401(k) plan, but it's important to understand how the matching works with each type of plan.

Employer contributions typically go into a traditional 401(k) account, so if you opt for a Roth 401(k), you won't receive the same tax benefits on those matching funds.

However, if your employer offers a Roth 401(k) and matches contributions to that account as well, you'll receive tax-free matching contributions.

Which Is The Best Option For You?

So, how do you decide which type of 401(k) is right for you? It really depends on your individual financial situation and goals. Here are some factors to consider:

Your current tax bracket: If you're in a high tax bracket now and expect to be in a lower bracket in retirement, a traditional 401(k) could be a good choice because you'll save money on taxes now.

Your expected tax bracket in retirement: If you expect to be in a higher tax bracket in retirement than you are.

What I Personally Use

I choose to utilize the Roth 401(k) option myself. I like the idea of paying taxes only on my invested income now vs paying much more in taxes on the contributions AND capital gains later.

I also love my Roth 401(k) because it’s the only way I can invest more money with great Roth tax incentives. The contribution limit for a Roth IRA is only $6,500 a year ($7,500 if age 50 or older), but utilizing a Roth 401(k) gives me an additional $22,500 to invest per year with the same tax benefits.

Also, my employer adds their matching contributions to my Roth 401(k) plan which means even more money growing tax-free. On top of that, I’m in a lower tax bracket now than I expect to be in when retiring. So for me personally, using the Roth 401(k) option makes the most sense.

Conclusion

Both 401(k) plans are decent options for the average person. They both offer the ability to passively invest for your future without needing to do much with your portfolio.

Choosing which option is best for you really comes down to your own unique financial situation. I personally love the Roth option for the reasons listed above as well as having a set tax rate that I can plan for.

Using a traditional 401(k) is fine too, but you have to assume your future tax rate (which is always subject to change) and that can potentially make it harder to plan for retirement.

Either plan will help you to prepare for retirement by setting up reoccurring investment contributions which is always a step in the right direction.

Thanks for reading and be sure to subscribe if you haven’t already!

Share this article with someone who you think it could help.

TIME TO UPGRADE?

Paid subscribers will receive an additional weekly newsletter called Mark Talks Markets on Fridays after the bell.

This special extra will give you up-to-date stock market news & insights complete with easy-to-understand technical analysis of the major stock indexes and Bitcoin each week.

With this added value, paid subscribers have the tools they need to make informed decisions about their investments and stay ahead of the curve.

Consider upgrading your plan to gain access to these additional weekly insights.

Great break down of both options. So glad I started this years ago and can watch the money grow.

Roth IRA’s print money!!